Mangoes

-

Marketing & export

As someone involved in Australian horticulture, it’s probably no surprise to you that export has been a major driver of industry growth over the last few years.

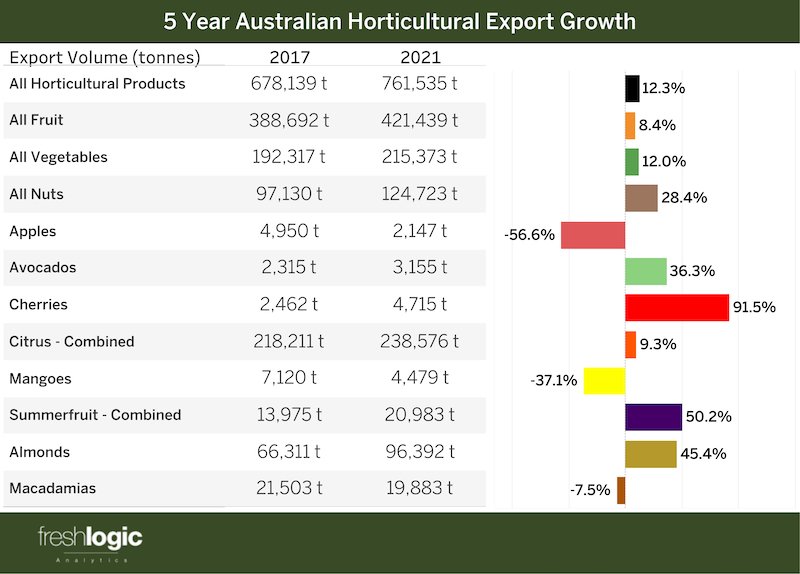

For the five-year period from June 2017–2021, export volume has grown by an additional 83,395 tonnes to 6,629,505 tonnes – an increase of 12.30% across all Australian horticulture categories.

This represents the highest growth in value across distribution channels, eclipsing value growth from total farm gate production (4.90%), retail (2.71%), and COVID-affected food service (-6.59%) sectors.

Tree crops are strongly represented among this export volume growth across key category lines, including avocados (+36%), cherries (+91.51%), citrus (+9.33%), summerfruit (+50.15%) and almonds (+45.36%)

These figures are even more impressive when accounting for challenges to export over 2021.

Due to record freight costs and limited shipping availability, significant volumes grown for export markets were not able to make it to their destination.

Additionally, logistical issues through Chinese ports have also posed a significant challenge for a number of products.

Considering its recent growth performance and an increasingly mature domestic market for many categories, export is now more than ever a vital channel for distribution systems of Australian crops.

Advantages for Australian exports

In the pursuit of export growth, there are several key advantages that Australia enjoys over its export competitors.

As a Southern Hemisphere exporter, counter-seasonality eliminates competition from more established Northern Hemisphere producers.

The proximity of a number of key Asian markets is also a significant advantage.

With rapidly increasing freight costs and freight availability issues globally, South American and Southern African exporters with longer supply chains are significantly more exposed, reducing competitiveness.

As a point of difference, the quality of Australian produce has also been historically acknowledged by trading partners through higher realised prices.

As an example, across 22 of Australia’s largest target export markets (ATEM), Australian mandarins return 69% above the average market value for 2020. This signals that trading partners recognise that a higher quality product will sell through.

As highlighted by Australia’s recent finalisation of a phytosanitary protocol for nectarines to Vietnam and reduction of tariffs on citrus to India, increasing market access is also allowing for greater diversification of product, reducing market risk and dependence.

Despite these relative export market advantages, with development now moving past the frontier stage, a greater understanding of competitors servicing these export markets will be required.

Key Southern Hemisphere export competitors

Of all products exported from the Southern Hemisphere annually, a small group of exporters dominate exports by volume.

For major export tree crop commodities, including almonds, apples, apricots, avocados, cherries, macadamias, mandarins, mangoes, nectarines, oranges, peaches and pears, exports are dominated by four exporters, Australia, Chile, Peru, South Africa and New Zealand.

Across the 22 ATEM markets for these tree crops, these four nations account for 1.85 millon export tonnes total in 2021. Chile is the largest of these, accounting for 40% of this volume, followed by South Africa 23.31%, Australia 15.21% and New Zealand at 9.43%.

Chile

Chile is the largest exporter in the Southern Hemisphere and a key exporter by volume for several temperate tree crops, including pome fruit, cherries, citrus and stonefruit.

Seasonally, Chile’s summer fruit begin export in large volumes in December, running at volume until early April.

This has provided an early window for Australian product in October/November for products such as stone fruit and cherries when seasonality permits. The winter citrus season also follows this pattern, with Chile’s orange season beginning in July.

Peru

While Peru has traditionally been an exporter of vegetable lines, including garlic and asparagus, it’s fruit exports have exploded in the 2010s, particularly for blueberries and table grapes servicing the US market.

For tree crops, Peru is a major exporter of avocados, mandarins and mangoes and were the largest Southern Hemisphere exporter to ATEM nations of avocados and mangoes.

Seasonally, Peru’s mango (Nov-April) and mandarin (April-November) seasons run for the same months as Australia. Avocados are produced in significant volumes from April to September.

South Africa

South Africa was the second largest exporter into ATEM trade partners in 2021, with major production of apples, pears, macadamias and oranges.

For oranges in particular, South Africa is by far the largest exporter in the Southern Hemisphere, with significant exports to European nations not captured by ATEM markets.

As a major exporter of oranges to Russia, it’s likely that a proportion of this additional export volume for the 2022 season will be diverted to ATEM, increasing competition within these markets as global trade sanctions continue.

New Zealand

A major world producer of apples, New Zealand also export significant volumes of cherries, avocados, mandarins and pears to ATEM.

As to be expected, seasonality of New Zealand tree crops mirrors those of Southern Australia. Additionally, with a similar reputation for safe, quality produce, New Zealand also tends to return pricing reflective of this acknowledgement.

Written by James Parry a market development manager for Freshlogic, a market research and analysis firm specialising in fresh food. James’ work assists to connect businesses with information and analysis to make more informed decisions. Get in contact at james.parry@freshlogic.com.au